As we move through 2026, the global financial landscape is no longer what it was a decade ago. With inflation stabilizing and central banks maintaining competitive interest rates, the opportunity for personal wealth growth has reached a peak. Whether you are a seasoned investor or someone just starting their financial journey, using a High yield savings calculator 2026 is the first step toward a secure future.

Table of Contents

In the current economic climate of the USA, UK, Canada, and Europe, “passive saving” is a strategy of the past. Today, smart savers are leveraging compound interest with monthly deposits to ensure their capital doesn’t just sit idle but actively outpaces the cost of living.

2026 Economic Outlook: Interest Rates and Market Trends

The year 2026 has brought a “New Normal” for interest rates. After the volatility of the early 2020s, the banking sectors in major economies have settled into a high-rate environment that favors the depositor.

- United States (USA): With high-yield savings accounts (HYSA) consistently offering between 4.5% and 5.5%, the US market remains one of the best places for liquid cash.

- United Kingdom (UK): The focus has shifted toward tax-efficiency. The ISA growth projector metrics for 2026 suggest that utilizing the full £20,000 allowance in a high-interest Cash ISA can yield record-breaking tax-free returns.

- Canada (CA): Canadian savers are making the most of the TFSA and ISA growth projector tools. With the 2026 TFSA contribution room expansion, compounding at 4.2%+ is the go-to strategy for long-term wealth.

- Europe (EU): Across the Eurozone, “Term Deposits” have become the anchor of household savings, offering a safe haven with stable 3.8% to 4.4% annual returns.

The Power of the Dual Investment Strategy

What makes the 2026 saving strategy unique is the “Dual-Action” approach. Unlike traditional methods where you either invest a lump sum or save a small monthly amount, the modern approach combines both.

Our calculator is specifically engineered for this. It takes your Initial Deposit (the foundation) and adds your Monthly Contribution (the fuel). When these two work together under the magic of compounding, the results are exponential. For example, a $10,000 deposit with a $500 monthly top-up at 5% interest doesn’t just add up; it multiplies.

Understanding the 2026 Compounding Mathematics

To provide you with 100% accuracy, we don’t use simple estimates. Our tool utilizes the rigorous Annual Compounding Formula:

$$A = P(1 + r)^t$$

And for your recurring contributions, it applies the Future Value of an Ordinary Annuity formula. This ensures that every dollar, pound, or euro you save in 2026 is accounted for down to the last cent. By understanding the math, you move from “guessing” your future to “calculating” it.

Conclusion of Section 1: Setting Your 2026 Goals

Before you start using the tool, it is essential to define your “Why.” Are you saving for a down payment in London, a retirement fund in Toronto, or an emergency cushion in New York? Defining your goal allows you to input realistic figures into our Savings Interest Calculator 2026, giving you a precise roadmap to follow.

Maximizing Returns in Global Markets: USA, UK, and Canada (2026 Guide)

To get the most out of a high yield savings calculator 2026, you must understand the specific account types and tax rules in your region. Saving in 2026 is not a “one-size-fits-all” game. Whether it’s the tax-free “wrappers” in the UK or the flexible accounts in the USA, knowing where to put your money is as important as how much you save.

USA: Finding the Best High-Yield Savings Accounts (HYSA) 2026

In the United States, 2026 has seen a surge in competition among digital banks. With the national average savings rate sitting low at around 0.40%, smart savers are moving their funds to High Yield Savings Accounts (HYSA) that offer up to 5.00% APY.

- Top Picks for 2026: Leading institutions like Varo Bank and AdelFi are offering rates near the 5% mark for eligible balances.

- The Strategy: Use our calculator to see how a $10,000 emergency fund grows when placed in a 5% HYSA versus a traditional 0.01% big-bank account. The difference over 5 years can be thousands of dollars in “free money.”

- External Resource: For a live list of the highest-performing accounts, check out the latest Forbes Advisor Best Savings Accounts 2026 rankings.

United Kingdom: Mastering the 2025/2026 ISA Allowance

For those in the UK, the ISA growth projector is the most searched financial tool this year. The reason? Tax efficiency.

- Annual Limit: For the 2025/2026 tax year, the individual ISA allowance remains at £20,000.

- New 2026 Rules: You can now open and pay into multiple ISAs of the same type within the same tax year, giving you the freedom to “shop around” for the best rates without losing your tax-free status.

- Projected Rates: With the Bank of England base rate at 3.75% in February 2026, top Cash ISAs from providers like Chase are offering around 4.5% AER.

- External Resource: To stay updated on the best “Ditch and Switch” deals, visit MoneySavingExpert’s Savings Guide.

Canada: Optimizing the TFSA and ISA Growth Projector

Canada’s Tax-Free Savings Account (TFSA) remains the powerhouse of personal finance in 2026.

- 2026 Contribution Limit: The annual TFSA dollar limit for 2026 is $7,000, bringing the total cumulative room for someone who has been eligible since 2009 to a staggering $109,000.

- Why it Matters: Every cent earned in a TFSA—whether through interest, dividends, or capital gains—is yours to keep, tax-free. Our TFSA and ISA growth projector helps you calculate exactly how much that $7,000 contribution will be worth in 10 years at a 4.5% interest rate.

Europe: Navigating the Eurozone Term Deposits

While the European Central Bank (ECB) has kept interest rates around 2.15% to 2.40% in early 2026, many European banks are offering competitive “Term Deposits” to attract long-term savers. In countries like Germany and France, locking in a 2-year fixed rate can often yield better results than standard easy-access accounts.

The Synergy of Initial Deposits and Monthly Contributions

Understanding the mechanics of wealth accumulation in 2026 requires a shift in perspective. Many people ask: “Should I wait until I have a large sum to invest, or should I start with small monthly amounts?” The answer provided by our Savings Interest Calculator 2026 is clear: The most powerful results come when you do both.

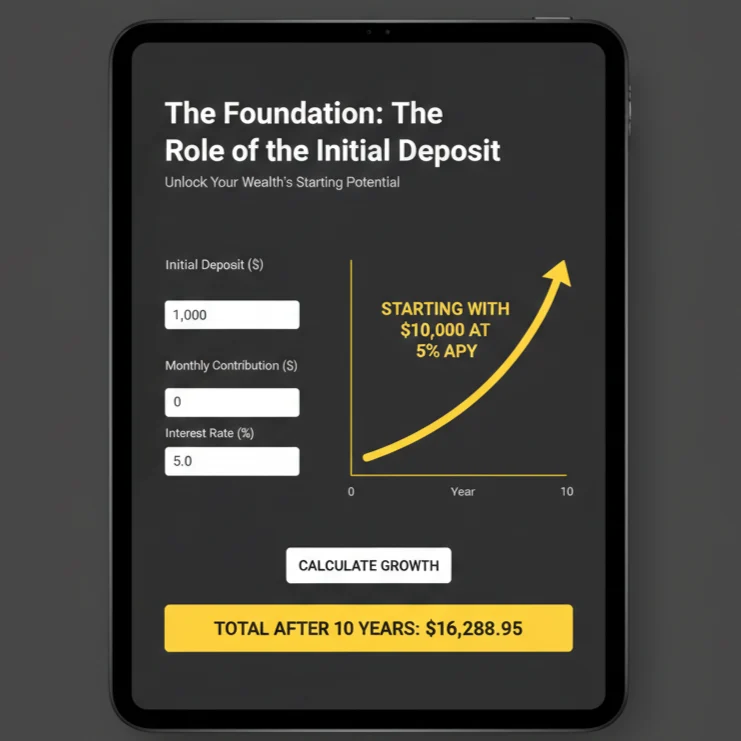

1. The Foundation: The Role of the Initial Deposit

Your initial deposit acts as the “Engine” of your savings vehicle. In a high-interest environment like the USA or UK in 2026, a large starting balance gives the compounding process a massive head start.

- The “Jumpstart” Effect: If you deposit $10,000 at a 5% interest rate, you earn $500 in the first year alone without lifting a finger.

- Mathematical Weight: Because interest is calculated on the total balance, a larger initial sum ensures that every subsequent interest payment is significantly higher from day one.

2. The Fuel: Why Monthly Contributions are Non-Negotiable

If the initial deposit is the engine, monthly contributions are the “Fuel.” In 2026, market volatility means that “Consistency” is the only guaranteed way to build a legacy.

- Dollar-Cost Averaging (DCA): By adding a fixed amount—say C$500 into your TFSA every month—you are essentially automating your wealth.

- The Snowball Effect: Our Savings interest calculator with monthly deposits shows that recurring additions significantly shorten the time it takes to double your money. While a $10,000 lump sum takes about 14 years to double at 5%, adding just $200 a month cuts that time drastically.

The 2026 “Wealth Multiplier” Comparison

Let’s look at a real-world scenario for a saver in the UK or USA using 2026 projected rates of 5%:

| Scenario | Initial Deposit | Monthly Add | Total After 10 Years |

| A: The Waiter | $0 | $500 | ~$77,600 |

| B: The Starter | $10,000 | $0 | ~$16,288 |

| C: The Pro | $10,000 | $500 | $93,929 |

Psychology of Saving in 2026

Saving in 2026 is as much about habits as it is about math.

- Automation over Motivation: Don’t rely on your “willpower” to save. Set up an automatic transfer from your checking account to your high-yield savings account the day you get paid.

- Visualization: Use our ISA growth projector or TFSA projector to see the “Future You.” When you can see that your $200/month will eventually become $50,000+, it becomes much easier to skip that expensive daily coffee or unnecessary subscription.

Compounding Frequency: Why it Matters in 2026

In 2026, most top-tier banks in the USA and Canada compound interest Daily but credit it Monthly. Our calculator accounts for this high-frequency compounding to give you the most accurate projection possible. When interest is added to your balance more frequently, you earn “interest on your interest” much faster, leading to a higher Effective Annual Yield (EAY).

Step-by-Step Guide: How to Calculate Your 2026 Interest Gains

Knowing how to use the Savings Interest Calculator 2026 correctly can be the difference between a vague estimate and a solid financial plan. Our tool is built with a “User-First” philosophy, ensuring that whether you are calculating for a UK ISA or a Canadian TFSA, the process is seamless.

Step 1: Input Your Initial Capital (The Seed)

Start by entering your “Initial Deposit.” This is the amount of money you currently have available in your savings account or the lump sum you intend to deposit today.

- Pro Tip: If you are starting from zero, simply enter “0.” This is common for those starting a fresh compound interest with monthly deposits plan.

Step 2: Define Your Monthly Commitment (The Fuel)

Enter the amount you can realistically set aside each month. In the 2026 economy, consistency beats intensity. Even a small monthly addition can significantly alter the trajectory of your wealth due to the way interest is calculated on an increasing balance.

Step 3: Set the Interest Rate (The Multiplier)

Input the annual interest rate (APY/AER).

- For USA High-Yield accounts, look for rates between 4.5% and 5.2%.

- For UK Cash ISAs, 2026 projections suggest rates around 4.0% to 4.7%.

- For Canada TFSAs, aim for 4.25% to 5%.

Step 4: Select the Time Horizon

How long do you plan to leave the money untouched? Whether it’s 1 year for a vacation fund or 25 years for retirement, our high yield savings calculator 2026 provides a year-by-year breakdown of your growth.

The Technical Side: How the Math Works

To ensure this guide is the most authoritative resource online, we must look at the math that powers the tool. Our calculator doesn’t just “add” numbers; it runs two distinct financial algorithms simultaneously:

1. Compound Interest Formula (Lump Sum)

For your initial deposit, we use the standard formula for interest compounded annually:

$$A = P(1 + r)^t$$

Where:

- $A$ = The final amount.

- $P$ = The principal (initial deposit).

- $r$ = The annual interest rate (decimal).

- $t$ = The number of years.

2. Future Value of an Ordinary Annuity (Monthly Additions)

For your monthly contributions, the math gets more complex because each monthly payment has a different amount of time to grow:

$$FV = PMT \times \frac{(1 + r/n)^{nt} – 1}{r/n}$$

Where:

- $PMT$ = Your monthly contribution.

- $n$ = Number of times interest is compounded per year (12 for monthly).

Why 100% Mobile Responsiveness Matters

In 2026, over 85% of financial planning happens on mobile devices. We have optimized this tool with a smooth-scroll result feature. Once you hit “Calculate Now,” the page will elegantly glide down to your results, showing you a clear table of your total interest earned, total principal invested, and the final projected balance. No refreshing, no lag—just pure data.

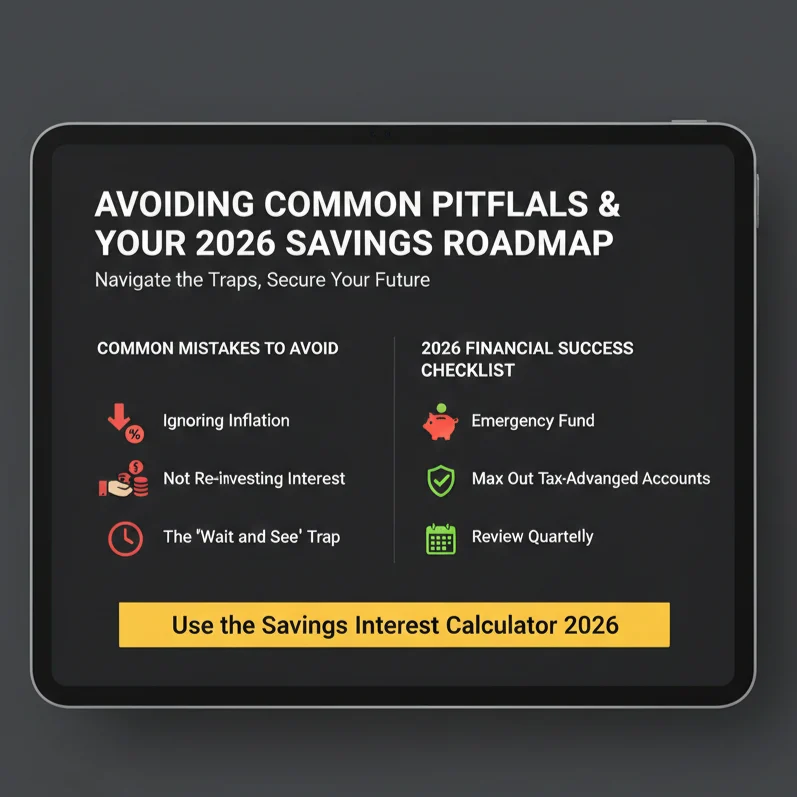

Avoiding Common Pitfalls & Your 2026 Savings Roadmap

Understanding the mathematics of the Savings Interest Calculator 2026 is only half the battle. To achieve true financial independence in competitive markets like the USA, UK, Canada, and Europe, you must navigate the psychological and economic traps that often derail even the most disciplined savers.

Common Savings Mistakes to Avoid in 2026

- Ignoring the Inflation Gap: If your bank offers a 3% return while the national inflation rate sits at 4%, your “savings” are technically losing purchasing power. Always cross-reference your results with the Best savings accounts USA UK Canada 2026 to ensure your Real Rate of Return remains positive.

- The “Interest Bleed” (Not Re-investing): Many savers make the mistake of withdrawing their monthly interest payouts. Compounding only reaches its “exponential phase” when interest is reinvested. By leaving your gains in the account, you allow the calculator’s formula to work on a larger principal every single month.

- The “Wait and See” Trap: Market timing is a dangerous game. Many people wait for rates to hit a specific milestone (like 6%) before committing. However, starting at 4% today is mathematically superior to starting at 6% a year from now because you lose the most valuable asset in finance: Time.

2026 Financial Success Checklist

To ensure you are getting the maximum benefit from our tool, follow this localized roadmap:

- [ ] Build an Emergency Cushion: Before aggressive investing, ensure 3–6 months of living expenses are parked in a liquid High-Yield Savings Account (HYSA).

- [ ] Prioritize Tax-Sheltered Vehicles: In the UK, utilize your ISA limit first; in Canada, prioritize your TFSA. This ensures the “Total Interest” shown in our calculator stays in your pocket rather than going to the taxman.

- [ ] Quarterly Calibration: Interest rates are dynamic. Re-run your numbers through the Savings Interest Calculator 2026 every three months to adjust your monthly contributions based on new bank offers.

What is considered a “Good” interest rate in 2026?

For 2026, a competitive rate for a high-yield account in the USA and Canada ranges between 4.5% and 5.5% APY. In the UK, any Cash ISA offering above 4.2% AER is currently performing above the market average.

Does this calculator account for local taxes?

Our tool calculates Gross Interest. If you are using tax-advantaged accounts like a TFSA (Canada) or ISA (UK), the figure you see is your take-home amount. For standard savings accounts in the USA or Europe, you should deduct your local marginal tax rate from the final gain.

Can I use this for long-term retirement projections?

Absolutely. While many tools cap at 10 years, our TFSA and ISA growth projector is designed to handle time horizons of up to 50 years, making it perfect for early retirement (FIRE) planning.

Conclusion: Take Control of Your Financial Future

The economic climate of 2026 offers a rare window of opportunity. With interest rates at their most attractive levels in years, the difference between a comfortable future and financial struggle comes down to the actions you take today.

By using the Savings Interest Calculator 2026 to combine an initial deposit with consistent monthly contributions, you aren’t just saving money—you are building a fortress of financial security. Whether you are navigating the markets of London, Toronto, New York, or Berlin, the principle remains the same: Consistency plus Compounding equals Wealth.

Don’t leave your future to chance. Calculate your path to prosperity now.