In the 2026 financial landscape, interest rate volatility has made it mandatory for homeowners to maintain a sharp eye on their home equity. Whether you are looking to lower your monthly mortgage payments or hoping to extract cash for home improvements, the first metric any lender will evaluate is your LTV ratio. Therefore, learning how to calculate loan to value is not just a mathematical exercise; it is a vital financial skill that can save you thousands of dollars over the life of your loan.

Table of Contents

The Mechanics of LTV and Risk Assessment

The Loan-to-Value (LTV) ratio is a critical risk assessment tool used by financial institutions globally. It represents the relationship between the amount of money you owe on a property and its current appraised market value. From a bank’s perspective, a higher LTV represents a higher risk of default. Conversely, a lower LTV indicates that the borrower has significant “skin in the game” (equity), which typically results in lower interest rates and better borrowing terms.

To understand how to calculate loan to value with precision, you can use the following standard formula:

$$LTV = \left( \frac{\text{Current Outstanding Loan Balance}}{\text{Appraised Fair Market Value of Property}} \right) \times 100$$

Practical Example:

Imagine your home in a major hub like London, Toronto, or New York is currently valued at $600,000. If your remaining mortgage balance is $420,000, your calculation would be:

$(420,000 / 600,000) \times 100 = \mathbf{70\%}$.

In the professional finance world, 70% is considered a very healthy ratio, often qualifying the homeowner for the best “tier-one” interest rates.

Free to use • Accurate 2026 Results • No Sign-up Required

Global Banking Benchmarks in 2026

Understanding how to calculate loan to value is essential because different countries have specific “thresholds” that trigger different costs:

- United Kingdom: Major lenders like Nationwide or Lloyds Bank use LTV “bands” (60%, 75%, 85%, and 90%). Crossing from 60.1% to 60% can drastically reduce your fixed-rate offer.

- United States: According to the Federal Housing Finance Agency (FHFA), once your LTV drops to 80%, you are legally entitled to request the removal of Private Mortgage Insurance (PMI), which can instantly save you hundreds of dollars every month.

- Canada: The CMHC requires mortgage default insurance for any LTV higher than 80%, meaning accurate calculation is the only way to avoid these hidden “high-ratio” costs.

How to Optimize Your LTV Ratio

If your current ratio is too high, you have two primary levers: increase the property’s value or decrease the debt balance. While market appreciation is often out of your control, reducing the debt is entirely within your power. This is where our loan overpayment calculator 2026 becomes indispensable. By making strategic extra payments, you accelerate the reduction of your principal balance, which in turn improves your LTV ratio and sets the stage for a much cheaper refinance in the future.

Technical Breakdown: How Student Loan Repayments are Calculated

Higher education debt is unique because, unlike a car loan or a credit card, it is often treated as a “social contract” between the government and the graduate. In 2026, as interest rates and cost-of-living metrics shift, it has become vital for professionals to understand exactly how student loan repayments are calculated. Knowing this number allows you to forecast your monthly cash flow and decide whether making voluntary overpayments is a better financial move than traditional investing.

The Methodology of Income-Contingent Repayment

In major economies like the UK, Australia, and parts of Europe, the calculation is not based on how much you borrowed, but on how much you earn. This is known as an Income-Contingent Loan (ICR). To grasp how student loan repayments are calculated, you must first identify your “Repayment Threshold”—the specific income level at which the government begins deducting payments from your salary.

The United Kingdom Perspective (Plan 2 & Plan 5): In the UK, the system is divided into several “Plans.” If you are on Plan 2 (those who started university between 2012 and 2023), the 2026 threshold is roughly £27,295 per year.

- The Formula: You pay 9% on any income earned above that threshold.

- Example: If your annual salary is £35,000, your repayment is calculated on £7,705 (£35,000 – £27,295).

- Annual Total: £693.45 (or roughly £58 per month).

For the most up-to-date figures, graduates frequently consult the Student Loans Company (SLC).

Free to use • Accurate 2026 Results • No Sign-up Required

The 2026 American Landscape: The SAVE Plan

In the United States, the methodology for how student loan repayments are calculated underwent a massive transformation with the introduction of the SAVE plan. Unlike previous models, the SAVE plan focuses on “Discretionary Income,” which is the difference between your Adjusted Gross Income (AGI) and 225% of the Poverty Guideline.

For many borrowers in 2026:

- Payment Caps: Monthly payments are capped at 5% to 10% of discretionary income.

- Interest Subsidies: If your calculated payment doesn’t cover the monthly interest, the government waives the remaining interest, preventing “ballooning” balances. To simulate your specific situation, the Federal Student Aid Estimator is the industry-standard tool for American borrowers.

Canada and the Global Prime Rate Influence

In Canada, the National Student Loans Service Centre (NSLSC) manages repayments. While the federal portion of Canadian student loans is currently interest-free, the provincial portions often carry a floating interest rate. Therefore, how student loan repayments are calculated in Canada involves a fixed monthly installment based on your loan’s “term” (usually 114 months), adjusted for the current Prime Rate.

Why Your Repayment Strategy Matters

Understanding these calculations is the first step toward financial freedom. If your mandatory repayment is low because of your income level, but the interest rate on the loan is high (as seen in some UK postgraduate loans or US private loans), your balance could actually be growing while you pay it.

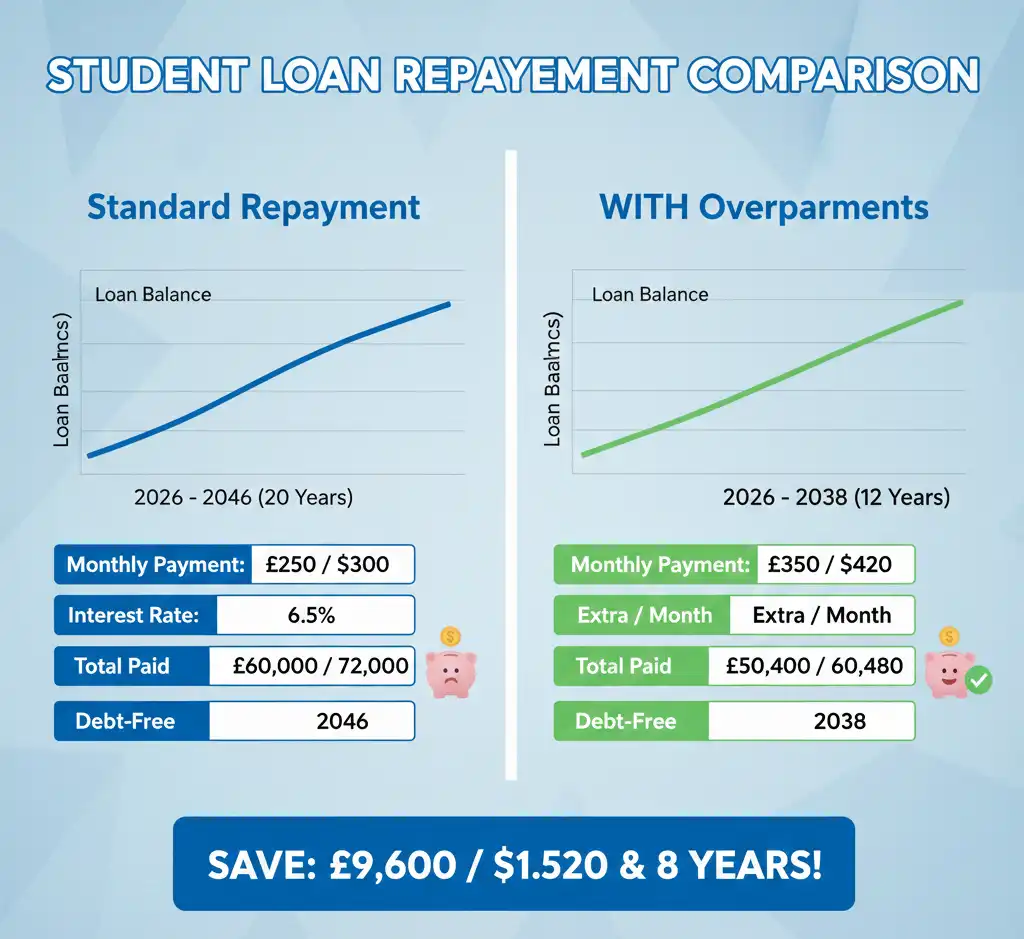

This is where a loan overpayment calculator 2026 becomes a game-changer. By entering your mandatory repayment and adding a “voluntary overpayment” amount, you can see how much faster you can kill the debt. Even a small $50 or £50 extra payment per month can potentially save you thousands in compounded interest and shave years off your repayment timeline.

Maximizing Financial Efficiency: The Role of a Loan Overpayment Calculator 2026

Once you have mastered the basics of how to calculate loan to value and have a clear forecast of how student loan repayments are calculated, the next logical step is to devise an exit strategy for your debt. In the economic climate of 2026, simply making the minimum required payments is often a slow path to financial freedom. Utilizing a professional-grade loan overpayment calculator 2026 allows you to see the “invisible” savings that occur when you prioritize debt reduction over traditional, low-yield savings accounts.

The Power of Principal Reduction

Every standard mortgage or student loan payment is split into two parts: Interest (the cost of borrowing) and Principal (the actual balance). In the early years of a 25 or 30-year term, a staggering amount of your money goes solely toward interest. This is a process known as amortization.

However, the “magic” happens when you make an overpayment. Because the lender has already received their scheduled interest from your regular payment, 100% of any extra money you contribute is applied directly to the Principal Balance. By using a loan overpayment calculator 2026, you can visualize how even a modest $150 or £100 monthly overpayment can trigger a “snowball effect,” drastically reducing the total interest the bank can charge you in subsequent months.

Why 2026 Demands a Strategic Approach

In 2026, we are seeing a “higher for longer” interest rate environment compared to the previous decade. Central banks, including the Federal Reserve and the Bank of England, have maintained baseline rates that make debt more expensive than ever.

- Guaranteed ROI: Paying off a loan with a 6.5% interest rate is mathematically identical to finding a guaranteed, tax-free investment return of 6.5%. In a volatile market, this is the safest “investment” a person can make.

- Shortening the Term: Our loan overpayment calculator 2026 helps you calculate your “Debt-Free Date.” For many homeowners, overpaying just 10% of their monthly installment can shave 6 to 8 years off a 30-year mortgage.

- LTV Optimization: As discussed in our section on how to calculate loan to value, overpaying your mortgage reduces your loan balance faster, which improves your LTV ratio and allows you to refinance into even cheaper interest rate tiers sooner.

Strategic Considerations for Global Borrowers

Before committing large sums to overpayments, it is essential to review your lender’s specific policies. For example, many banks in Canada and the UK, such as Royal Bank of Canada (RBC) or Barclays, allow an annual overpayment of up to 10% of the original loan balance without triggering “Early Repayment Charges” (ERCs).

By integrating the data from your current statements into our loan overpayment calculator 2026, you gain the clarity needed to decide whether to invest your surplus cash in the stock market or to secure a guaranteed win by crushing your debt.

Advanced Refinancing Strategies: Leveraging LTV to Secure 2026 Lower Rates

Once you understand how to calculate loan to value, you realize that this ratio is not static—it is a moving target that you can actively influence to save money. In 2026, refinancing has become a strategic game of “LTV Banding.” If your LTV is sitting at 76%, you are likely paying a higher interest rate than someone at 75%. This section explores how to bridge that gap and why it is the most effective way to lower your cost of debt.

The “LTV Banding” Secret of Modern Lenders

Lenders categorize risk into specific buckets or “bands.” Typically, these bands are 90%, 80%, 75%, and the “Gold Standard” of 60%. If you are looking to refinance, your primary goal should be to push your ratio into a lower band before you apply.

For example, if you have been making regular payments and your home has increased slightly in value, your LTV might have naturally dropped from 85% to 81%. However, staying at 81% is a financial mistake. By using a loan overpayment calculator 2026 to find the exact amount needed to reach 79%, you can cross the 80% threshold. In the USA, this doesn’t just lower your rate; it also triggers the removal of Private Mortgage Insurance (PMI) as per Consumer Financial Protection Bureau (CFPB) guidelines.

Strategies to Rapidly Lower Your LTV Ratio

If you find that your current calculation for how to calculate loan to value is higher than you’d like, consider these three professional maneuvers:

- Strategic Capital Injection: Use a lump-sum payment (bonus, tax refund, or savings) to pay down the principal balance. Before doing so, run the numbers through our loan overpayment calculator 2026 to see if that payment moves you into a lower interest rate band.

- Appraisal Management: In 2026, the property market is localized. If you’ve made improvements to your home (like solar panels or an ADU), request a fresh appraisal. A higher home value instantly lowers your LTV, even if your loan balance stays the same.

- The “Recast” Option: Some lenders in the US and Canada allow for a “Mortgage Recast.” This is where you pay a large sum toward the principal, and the lender re-amortizes your loan based on the new, lower balance. This keeps your interest rate the same but lowers your monthly commitment.

Why LTV and Student Loans Intersect

Interestingly, your LTV can affect your ability to manage other debts, like student loans. Many homeowners use a “Cash-Out Refinance” to pay off high-interest student debt. To do this safely, you must know how to calculate loan to value to ensure you don’t exceed 80% LTV, which would make your mortgage significantly more expensive.

If your how student loan repayments are calculated shows that you are paying 7% or 8% interest, but you can refinance your home at 5% while keeping a 70% LTV, consolidating that debt could save you hundreds of dollars in monthly cash flow. However, this move should only be made after careful simulation using our loan overpayment calculator 2026 to ensure the long-term interest costs don’t outweigh the short-term monthly savings.

The 2026 Global Refinancing Outlook

In Europe and the UK, the European Central Bank (ECB) and the Bank of England have introduced stricter “Affordability Stress Tests.” This means that even if you have a great LTV, you still need to prove your income can handle the rates. Proper documentation of your student loan obligations is key here, as lenders will look at how student loan repayments are calculated against your gross income to determine your Debt-to-Income (DTI) ratio.

2026 Global Economic Trends: Future-Proofing Your Debt Strategy

As we move through 2026, the global financial landscape has shifted into a “New Normal.” The era of ultra-low interest rates is behind us, and borrowers in the USA, UK, Canada, and Europe are facing a market where precision matters more than ever. To thrive in this environment, understanding how to calculate loan to value and keeping a close watch on how student loan repayments are calculated is no longer optional—it is a requirement for survival.

Free to use • Accurate 2026 Results • No Sign-up Required

The Rise of “Smart Debt” Management

In the past, debt was something you simply paid off over 30 years. Today, savvy borrowers treat their debt as a portfolio. By using a loan overpayment calculator 2026, individuals are now “arbitraging” their debt. This means they are choosing to pay down high-interest liabilities while maintaining low-interest assets.

For example, if you have a student loan with a variable rate that has climbed to 7%, but your mortgage is locked in at 4%, the math is clear: every extra dollar should go toward the student loan. Our loan overpayment calculator 2026 helps you prioritize which debt to attack first by showing you the “Total Interest Saved” for each scenario.

Regional Forecasts for 2026 and Beyond

- United States: The Federal Reserve has signaled a focus on long-term stability. This means LTV ratios will remain the primary gatekeeper for the best rates. Homeowners are encouraged to keep their LTV below 75% to navigate potential housing market corrections.

- United Kingdom: With the “Plan 5” student loans fully integrated, the way how student loan repayments are calculated in the UK now leans more heavily on lower-income earners. Graduates must be more proactive with overpayments to avoid carrying debt into their 50s.

- Canada: The Canadian market is seeing a trend toward “Accelerated Bi-Weekly” payments. By adjusting your payment frequency, you effectively make one extra month’s payment every year, which works exactly like the overpayment strategies simulated in our calculator.

The Psychology of Financial Freedom

Beyond the numbers, the psychological impact of debt reduction is profound. Study after study shows that reducing debt levels significantly lowers cortisol (the stress hormone) and improves long-term decision-making. Whether you are improving your equity by learning how to calculate loan to value or finally understanding the deductions on your payslip through how student loan repayments are calculated, you are taking back control of your time.

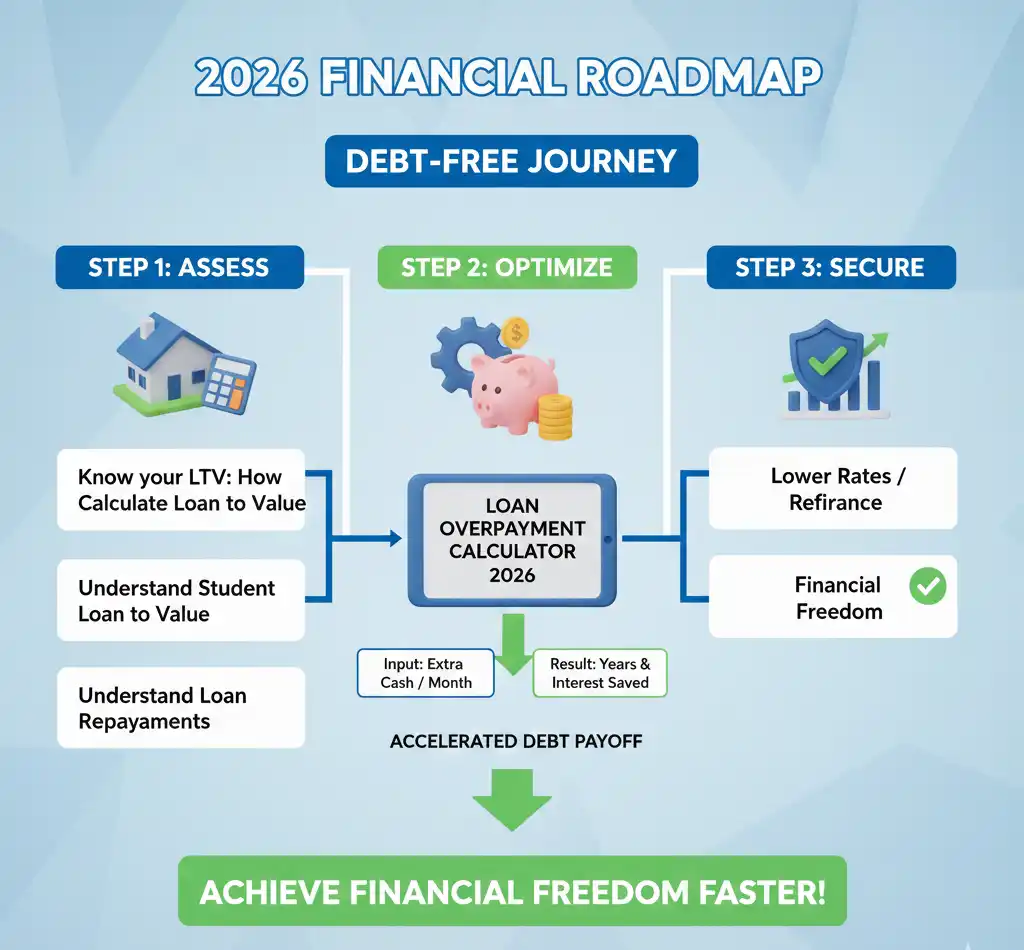

Conclusion: Your Roadmap to a Debt-Free Life

The journey to financial independence in 2026 is built on three pillars:

- Assessment: Knowing exactly where you stand by calculating your LTV and DTI ratios.

- Education: Understanding the specific rules governing your student and mortgage debt.

- Action: Using tools like the loan overpayment calculator 2026 to make informed, data-driven decisions.

By consistently overpaying even small amounts and monitoring your LTV bands, you aren’t just paying off a loan—you are buying back your future.

Frequently Asked Questions (FAQs)

What is the easiest way how to calculate loan to value?

The easiest way is to divide your current mortgage balance by the appraised market value of your property and multiply by 100. For example, if you owe $300,000 on a $400,000 house, your LTV is 75%. This ratio is critical for 2026 refinancing rates.

How student loan repayments are calculated in the UK for 2026?

In the UK, repayments are calculated as 9% of your income above a specific threshold. For Plan 2 graduates in 2026, this threshold is approximately £27,295. If you earn below this, you don’t pay anything, but interest still accrues on your balance.

Can I use a loan overpayment calculator 2026 for student loans?

Yes, you can. While student loan repayments are automatic, making voluntary overpayments can save you thousands in interest. Using a loan overpayment calculator 2026 helps you see how much earlier you could clear the debt and if it’s more beneficial than traditional saving.

Why does my LTV matter when I refinance?

LTV matters because it determines your interest rate “band.” Lenders offer much lower rates for LTVs under 60% or 75%. If you know how to calculate loan to value accurately, you can make a small overpayment to drop into a lower band and secure a cheaper mortgage.

How student loan repayments are calculated for US SAVE plans?

For the US SAVE plan, repayments are calculated based on your Discretionary Income (the amount you earn above 225% of the Poverty Guideline). You typically pay 5% to 10% of this income, and any remaining monthly interest is waived by the government.

Is overpaying a loan better than investing in 2026?

It depends on your interest rate. If your loan rate is 6% or higher, overpaying provides a “guaranteed” return of 6% tax-free. Our loan overpayment calculator 2026 can help you compare the total interest saved versus potential market gains.