PAYE Salary Calculator

UK Tax Year 2026 / 2027 Estimates

The Evolution of UK Taxation in 2026

The financial landscape for workers in the United Kingdom is constantly shifting, and 2026 is no exception. As we navigate through new fiscal policies and economic adjustments, understanding the granular details of your payslip has become more important than ever. For the average employee, the difference between gross pay and net income can be quite substantial, which is why having access to a precise UK PAYE Salary Calculator 2026 is vital for effective household budgeting.

The “Pay As You Earn” (PAYE) system is the primary method used by HM Revenue and Customs (HMRC) to collect Income Tax and National Insurance directly from your wages. While this system is designed to be seamless, it often leaves workers wondering how their final take-home pay was determined. By utilizing our updated UK PAYE Salary Calculator 2026, you can demystify these calculations. This tool takes into account all the latest thresholds and rates set for the current tax year, ensuring that you aren’t left with any unexpected financial surprises at the end of the month.

Understanding the Shift in National Insurance

One of the most significant changes for the 2026/27 period is the stabilization of National Insurance contributions. After years of fluctuating rates, the current 8% rate for Class 1 contributions has provided some predictability for the workforce. When you input your details into the UK PAYE Salary Calculator 2026, it automatically factors in this 8% deduction alongside the standard tax bands. This level of detail is essential for anyone looking to compare job offers or plan for long-term savings goals.

Why Transparency Matters in Payroll

Transparency in payroll isn’t just about knowing how much you earn; it’s about understanding your contribution to the public system. The taxes collected via the PAYE framework fund essential services like the NHS, education, and infrastructure. However, as a taxpayer, you have the right to ensure you aren’t overpaying. Using a reliable UK PAYE Salary Calculator 2026 allows you to cross-verify your employer’s figures with the official HMRC Income Tax standards.

This section of our guide aims to provide the foundational knowledge needed to navigate these fiscal waters. As we move deeper into the specific mechanics of tax codes and personal allowances in the following chapters, remember that the goal is financial empowerment. EveryToolHub is committed to providing the most user-friendly experience, ensuring that every worker in the UK can access their financial data with a single click.

Decoding Tax Codes and Your Personal Allowance

Understanding your tax code is arguably the most critical step in ensuring you are paid correctly. On most UK payslips, you will see a combination of numbers and letters, such as 1257L. This code is what your employer uses to determine how much income is handed over to HMRC and how much stays in your pocket. While many people use the UK PAYE Salary Calculator 2026 to get a quick estimate, knowing the logic behind these codes can help you spot errors that might be costing you hundreds of pounds a year.

The numerical part of the code (like 1257) usually represents your tax-free Personal Allowance. By adding a zero to the end of this number, you get the total amount you can earn before Income Tax kicks in—currently £12,570 for the 2026/27 tax year. The letters, however, provide specific instructions to your payroll department. For instance, the letter ‘L’ is the most common and indicates that you are entitled to the standard Personal Allowance. If you notice a different letter, such as ‘BR’ or ‘K’, your take-home pay will vary significantly from the standard results of a UK PAYE Salary Calculator 2026.

Common Tax Code Letters Explained

To give you a better perspective, here is a breakdown of what the most frequent letters mean:

- L: You are entitled to the standard tax-free Personal Allowance (£12,570).

- BR: Standing for “Basic Rate,” this means all your income from this specific job is taxed at 20% with no tax-free allowance. This usually happens if you have a second job.

- K: This is a “negative allowance” code. It means you have untaxed income from elsewhere (like company benefits) that is greater than your allowance.

- M & N: These relate to the Marriage Allowance, where you have either received or transferred 10% of a Personal Allowance to a spouse.

Why Your Code Might Change in 2026

Your tax code is not permanent. HMRC may update it if you start receiving company benefits like a car or health insurance, or if you begin receiving a pension. When these changes happen, using the UK PAYE Salary Calculator 2026 becomes even more important. It allows you to simulate your new net pay by adjusting the tax code field to match your new coding notice.

Emergency tax codes are another common occurrence, often appearing as “1257L W1” or “1257L M1.” These are temporary codes used when HMRC does not have enough information about your previous earnings. While they still provide a Personal Allowance, they calculate tax only on that specific pay period rather than your year-to-date earnings. If you find yourself on an emergency code, cross-referencing your payslip with a UK PAYE Salary Calculator 2026 can help you estimate the potential refund you might be owed once your records are updated by HMRC.

The Impact of Incorrect Coding

The danger of an incorrect tax code is either overpaying tax and being short on cash, or underpaying and facing a large bill later. For higher earners making over £100,000, the Personal Allowance actually begins to disappear—reducing by £1 for every £2 earned above that threshold. This “taper” is a complex calculation that many people struggle with, but our tools are designed to handle these nuances. By regularly checking your status, you ensure that your financial planning remains on track for the entire 2026/27 period.

Beyond Income Tax, the two most significant deductions on any UK payslip are National Insurance (NI) and workplace pension contributions. For many, these figures can be confusing, especially since they are calculated differently than standard tax. While you might use a UK PAYE Salary Calculator 2026 to see the final result, understanding the “how” and “why” behind these numbers is essential for long-term financial health. National Insurance is not just a tax; it is a contribution that builds your entitlement to certain state benefits, most notably the State Pension.

In the 2026/27 tax year, the Primary Threshold for National Insurance is aligned with the Personal Allowance at £12,570 per year. This means you only start paying the main rate of NI—currently 8% for most employees—once your earnings exceed this limit. However, unlike Income Tax, NI is calculated on a “per pay period” basis rather than a cumulative annual basis. This nuance is why people often see fluctuations in their net pay if they receive a bonus or work overtime in a specific month. Our UK PAYE Salary Calculator 2026 handles these variables seamlessly, giving you a projection based on your total annual earnings.

The Role of Auto-Enrolment Pensions

Since the introduction of auto-enrolment legislation, almost every worker in the UK is now part of a workplace pension scheme. By default, the minimum total contribution is 8% of your “qualifying earnings.” Usually, this is split as 5% from the employee and 3% from the employer. It is important to note that your 5% contribution actually feels like 4% because the government adds 1% in the form of tax relief. When you evaluate your take-home pay using a UK PAYE Salary Calculator 2026, you must consider whether your pension is deducted before or after tax is calculated.

There are two main ways pension contributions are handled:

- Net Pay Arrangement: Your pension is taken from your salary before Income Tax is calculated. This lowers your taxable income, meaning you pay less tax overall.

- Relief at Source: Your pension is taken from your salary after tax has been paid. Your pension provider then claims the basic rate tax relief back from HMRC and adds it to your pension pot.

Optimizing Your Net Pay with Salary Sacrifice

A growing number of employers now offer “Salary Sacrifice” for pension contributions. This is a highly tax-efficient arrangement where you formally agree to reduce your salary by the amount of your pension contribution. In return, your employer pays that same amount directly into your pension. Because your official salary is lower, both you and your employer pay less National Insurance. For higher-rate taxpayers, this can result in significant savings that a standard UK PAYE Salary Calculator 2026 might not show unless specifically configured for salary sacrifice.

Planning for the Future

While opting out of a pension might increase your immediate cash flow, you lose out on ‘free money’ from employer contributions and tax relief. Experts recommend using a UK PAYE Salary Calculator 2026 to see how small contribution changes impact your budget without sacrificing your future. For 2026/27, mandatory employer contributions are capped at £50,270 unless your contract states otherwise. Staying informed with the right tools ensures you balance today’s needs with tomorrow’s retirement security.

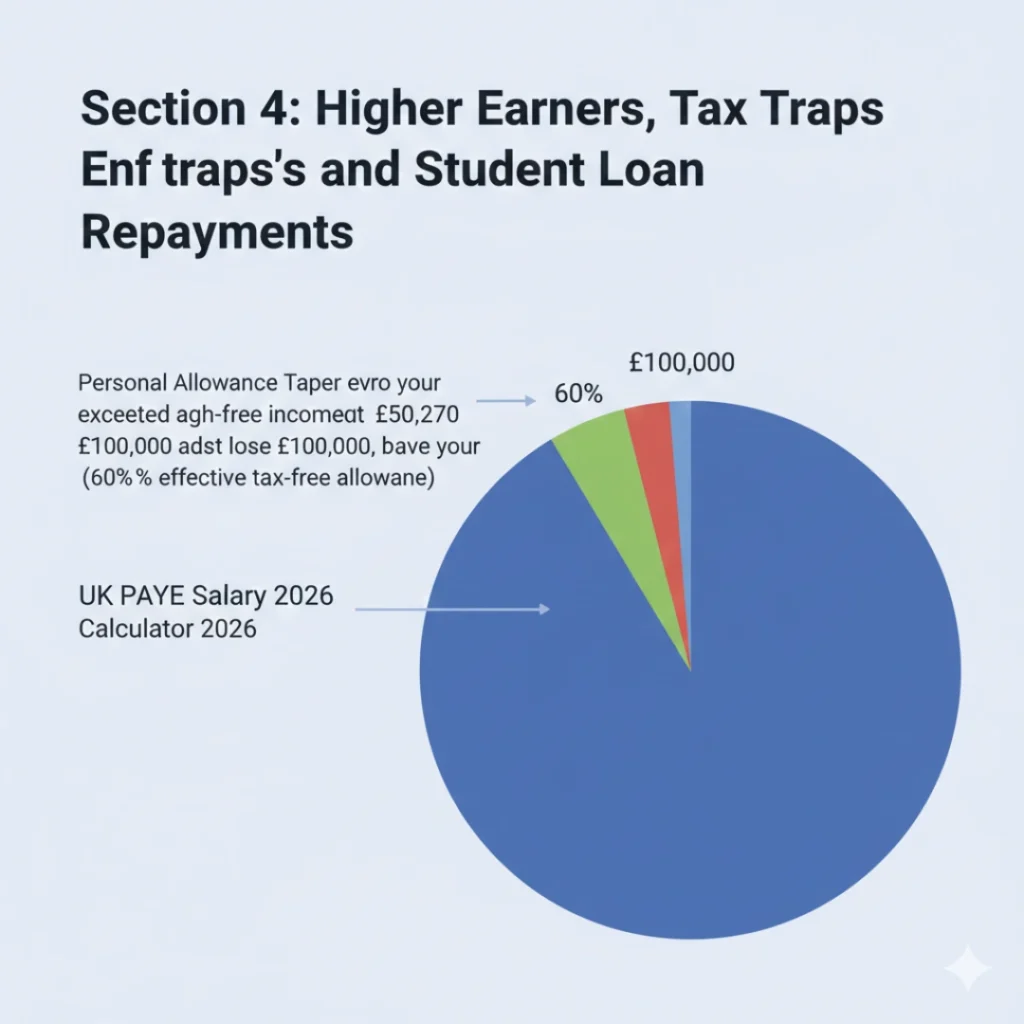

Higher Earners, Tax Traps, and Student Loan Repayments

As your career progresses, UK tax thresholds like ‘fiscal drag’ can make pay rises less impactful than expected. Moving from the 20% Basic Rate to the 40% Higher Rate at £50,270 is a major shift, but the most daunting challenge is the ‘60% tax trap.’ This occurs above £100,000, where you lose £1 of your Personal Allowance for every £2 earned. Using a UK PAYE Salary Calculator 2026 is the only way to accurately visualize these complex tapers. To avoid this 60% effective tax, many professionals use our UK PAYE Salary Calculator 2026 to plan pension contributions that keep their taxable income below the £100k limit.

The Impact of Student Loan Deductions

For many graduates, Student Loan repayments represent a “hidden tax” that significantly reduces their monthly net pay. In the 2026/27 tax year, repayments are generally calculated at 9% of your income above a specific threshold, depending on your plan:

- Plan 1: For those who started university before 2012.

- Plan 2: For those who studied between 2012 and 2023.

- Plan 5: The newest plan for recent students with a lower repayment threshold.

When you combine a 40% tax rate, 8% National Insurance, and a 9% Student Loan deduction, a higher-rate taxpayer can see a marginal tax rate of 57%. This is why the UK PAYE Salary Calculator 2026 is such an essential tool; it allows you to see the cumulative effect of these various deductions simultaneously. Understanding these figures is vital when considering whether to work overtime or take on additional responsibilities that might push you into a higher repayment bracket.

Child Benefit and High Income Charges

Another area where higher earners are often caught out is the High Income Child Benefit Charge. If you or your partner earns over £60,000 (thresholds may vary by 2026), you may have to pay back some or all of the Child Benefit you receive through your tax return. While this isn’t always deducted directly through PAYE, it is a critical factor in your overall financial health. By using the UK PAYE Salary Calculator 2026 to determine your “Adjusted Net Income,” you can plan ahead for these tax year-end liabilities.

External Resource: Repaying your student loan – Official Rules

Navigating these thresholds requires proactive planning. Whether you are dealing with the £100k taper, student loan plans, or benefit charges, the goal is to have no surprises when your payslip arrives. The UK PAYE Salary Calculator 2026 serves as your first line of defense in understanding these professional-level tax challenges, ensuring that you can make informed decisions about your career and your contributions to your workplace pension or other tax-efficient schemes.

Strategic Financial Planning for the 2026/27 Tax Year

Mastering your finances starts with having the right data at the right time. As we have explored in the previous sections, the UK tax system is a multi-layered structure of allowances, bands, and mandatory contributions. While the technical side of taxes can be overwhelming, the practical application of this knowledge is where the real benefit lies. By consistently using the UK PAYE Salary Calculator 2026, you aren’t just looking at numbers; you are creating a roadmap for your financial future. Whether you are saving for a mortgage, planning a family, or looking to invest, knowing your exact net income is the foundation of every successful budget.

Building a Robust Monthly Budget

Once you have determined your take-home pay using the UK PAYE Salary Calculator 2026, the next step is effective allocation. Financial experts often suggest the 50/30/20 rule: 50% of your net income for needs (rent, bills, food), 30% for wants, and 20% for savings or debt repayment. However, in high-cost areas of the UK, these percentages might need adjusting. The beauty of the UK PAYE Salary Calculator 2026 is that it allows you to see your income in monthly and weekly formats, making it much easier to align your earnings with your direct debits and standing orders.

Proactive Tax Management

One of the most overlooked aspects of being a PAYE employee is the ability to influence how much tax you pay. Through legal and government-approved schemes, you can often increase your take-home value or long-term wealth. Some of these include:

- Cycle to Work Scheme: Buying a bike through your employer can save you significant amounts on Tax and NI.

- Charitable Giving (GAYE): Donating to charity directly from your gross pay is highly tax-efficient.

- Marriage Allowance: If your partner earns less than the personal allowance, they can transfer a portion to you.

Before committing to any of these, it is wise to run the numbers through a UK PAYE Salary Calculator 2026 to see exactly how your monthly “bottom line” will change. Even a small adjustment in your tax code or a minor salary sacrifice can result in hundreds of pounds saved over the course of the fiscal year.

Why EveryToolHub is Your Long-term Partner

Our commitment at EveryToolHub goes beyond just providing a one-time calculation. We aim to be a continuous resource as the economic climate evolves. As the government announces new budgets or adjustments to the National Insurance framework, we update the UK PAYE Salary Calculator 2026 immediately. This ensures that you always have access to the most current information without having to read through lengthy legislative documents.

In conclusion, while the UK tax system is undoubtedly complex, tools like the UK PAYE Salary Calculator 2026 put the power back into the hands of the taxpayer. Financial literacy is a journey, and by understanding your deductions—from Income Tax and NI to Student Loans and Pensions—you are taking the first step toward total financial control. Bookmark our UK PAYE Salary Calculator 2026 and use it as your go-to reference for every pay rise, job change, or budget review in the 2026/27 tax year.

Frequently Asked Questions (FAQs)

1. What is the standard tax code for 2026/27?

The most common tax code is 1257L, which gives you a tax-free Personal Allowance of £12,570. Our UK PAYE Salary Calculator 2026 uses this as the default to estimate your net pay accurately.

2. How much is National Insurance (NI) in 2026?

For the 2026/27 tax year, the Class 1 National Insurance rate is 8% for most employees. The UK PAYE Salary Calculator 2026 automatically applies this rate to your earnings above the £12,570 threshold.

3. What is the 60% tax trap?

The 60% tax trap occurs when you earn over £100,000, as you lose £1 of Personal Allowance for every £2 earned. You can use the UK PAYE Salary Calculator 2026 to see how this affects your take-home pay and plan pension contributions to avoid it.

4. Can I calculate second job tax?

Yes. If you have a second job, change the tax code in our UK PAYE Salary Calculator 2026 to BR (Basic Rate). This ensures the tool calculates tax at 20% on all earnings without applying the personal allowance twice.

5. Does this tool include Student Loan repayments?

This UK PAYE Salary Calculator 2026 focuses on Income Tax and NI. However, it shows your taxable income, which is the base for the 9% Student Loan deduction (depending on your Plan).

Explore More Free Tools on EveryToolHub (2026 Edition)

Explore More Free Tools