“To answer the question of what is buy to let mortgage repayment, we must look at how lenders assess rental income. In 2026, banks in the UK, USA, and Canada use this calculation to decide if your property is a viable investment or a financial risk.”

The global real estate investment landscape in 2026 has transitioned into a highly regulated and data-driven environment. For investors targeting lucrative markets in the United Kingdom, United States, Canada, and Europe, the primary question remains: What is buy-to-let mortgage repayment? To put it simply, a Buy-to-Let (BTL) mortgage repayment is the financial obligation an investor undertakes when borrowing capital to purchase a property specifically for the purpose of renting it out.

Table of Contents

Unlike traditional residential mortgages, where approval is based on your personal salary and creditworthiness, BTL repayments are fundamentally tied to the “Rental Yield” of the asset. In 2026, lenders have become more stringent, often requiring a “Rental Cover” that ensures the expected rent exceeds the mortgage repayment by a significant margin (usually 125% to 145%).

Why Strategic Calculation is Critical

With the fluctuations in global interest rates witnessed early this year, guessing your monthly costs is a recipe for financial disaster. Investors now rely on advanced digital tools to forecast their liabilities. Using a specialized Buy to Let Mortgage Repayment Calculator 2026 allows you to input various variables such as property value, deposit size, and interest rates to see exactly how your cash flow will look.

According to the latest financial stability reports from the Bank of England, the ability of a property to “pay for itself” is the number one metric for loan approval. If your repayment structure isn’t optimized, you could face “negative carry,” where your outgoings exceed your rental income, effectively draining your personal savings instead of building wealth.

The Pillars of a BTL Repayment Plan

To truly understand the “what” of this process, one must look at the three pillars that define every repayment plan:

- The Capital: The actual sum borrowed.

- The Interest Margin: The profit the bank makes on your loan.

- The Amortization Period: The lifespan of the loan, which dictates the size of each installment.

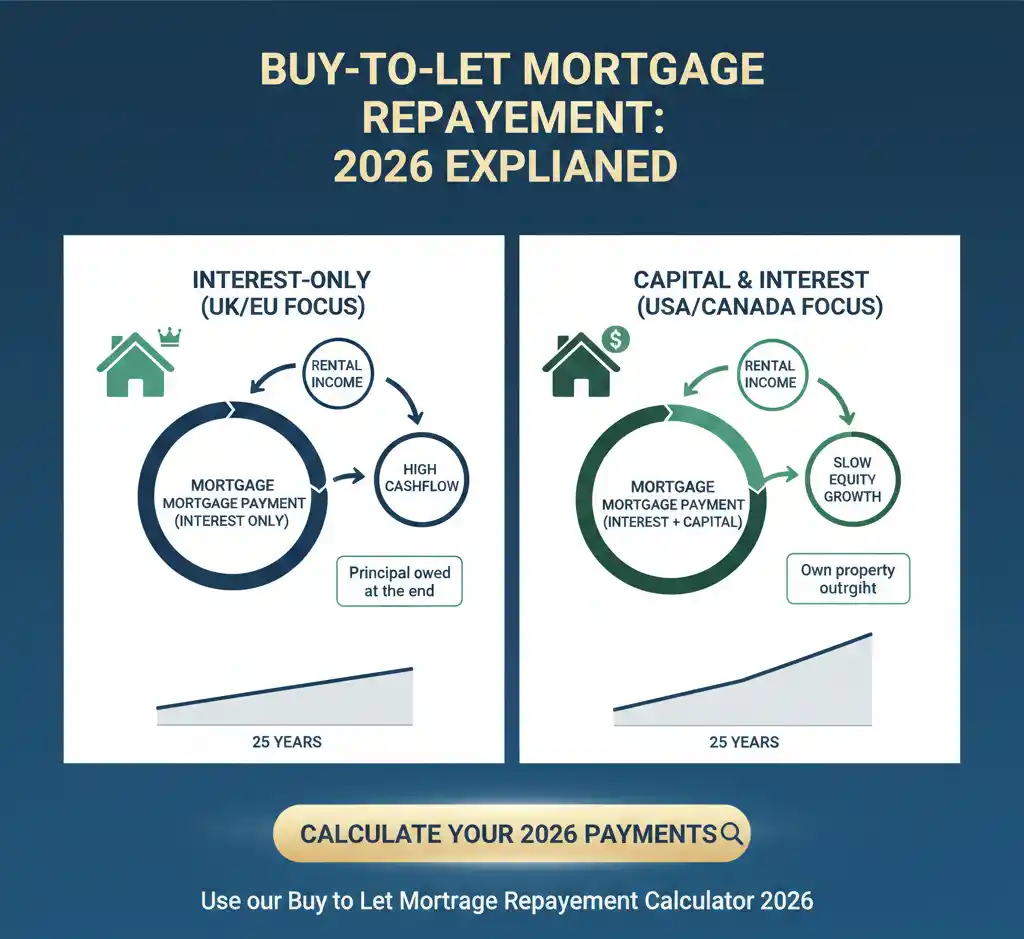

Comparing Repayment Methods (Interest-Only vs. Capital)

In 2026, investors generally choose between two distinct repayment structures. The choice you make here will define your tax efficiency and your monthly “take-home” profit.

1. Interest-Only Repayment Models

This is the most common strategy for professional investors in the UK and Europe. Under this model, your monthly payment covers only the interest charged on the loan. The original principal amount remains untouched.

- The Advantage: It maximizes monthly cash flow, allowing investors to save for their next property deposit.

- The Risk: You still owe the full loan amount at the end of the term, requiring a robust “exit strategy,” such as selling the property or refinancing.

2. Capital and Interest (Full Amortization)

Preferred by conservative investors in the USA and Canada, this method involves paying back both the interest and a portion of the principal every month.

- The Advantage: You are building equity. By the end of the term, you own the property outright.

- The Risk: Monthly repayments are significantly higher, which can squeeze your profit margins in high-interest-rate environments.

The Mathematics of 2026 Repayments

To calculate the exact repayment for a capital and interest loan, the industry standard formula is:

$$M = P \frac{r(1+r)^n}{(1+r)^n – 1}$$

While this formula provides the raw data, modern investors prefer integration with high-authority financial platforms like Bloomberg Wealth and our own Buy to Let Mortgage Repayment Calculator 2026 to account for hidden costs like property taxes and maintenance reserves. Understanding these types of repayments is the first step in ensuring your 2026 portfolio remains resilient against inflation and market shifts.

A Detailed Look: What is buy to let mortgage repayment?

“To answer the question of what is buy to let mortgage repayment, we must look at how lenders assess rental income. In 2026, banks in the UK, USA, and Canada use this calculation to decide if your property is a viable investment or a financial risk.”

Global Regulatory Landscapes and Tax Implications in 2026

The year 2026 has brought significant shifts in how governments perceive rental income and mortgage debt. As an investor, you cannot look at a buy-to-let mortgage repayment in isolation; you must consider the regulatory environment of the specific country where the asset is located. These laws directly impact your “Net Yield” and how much of your rental income actually stays in your pocket after the repayment is made.

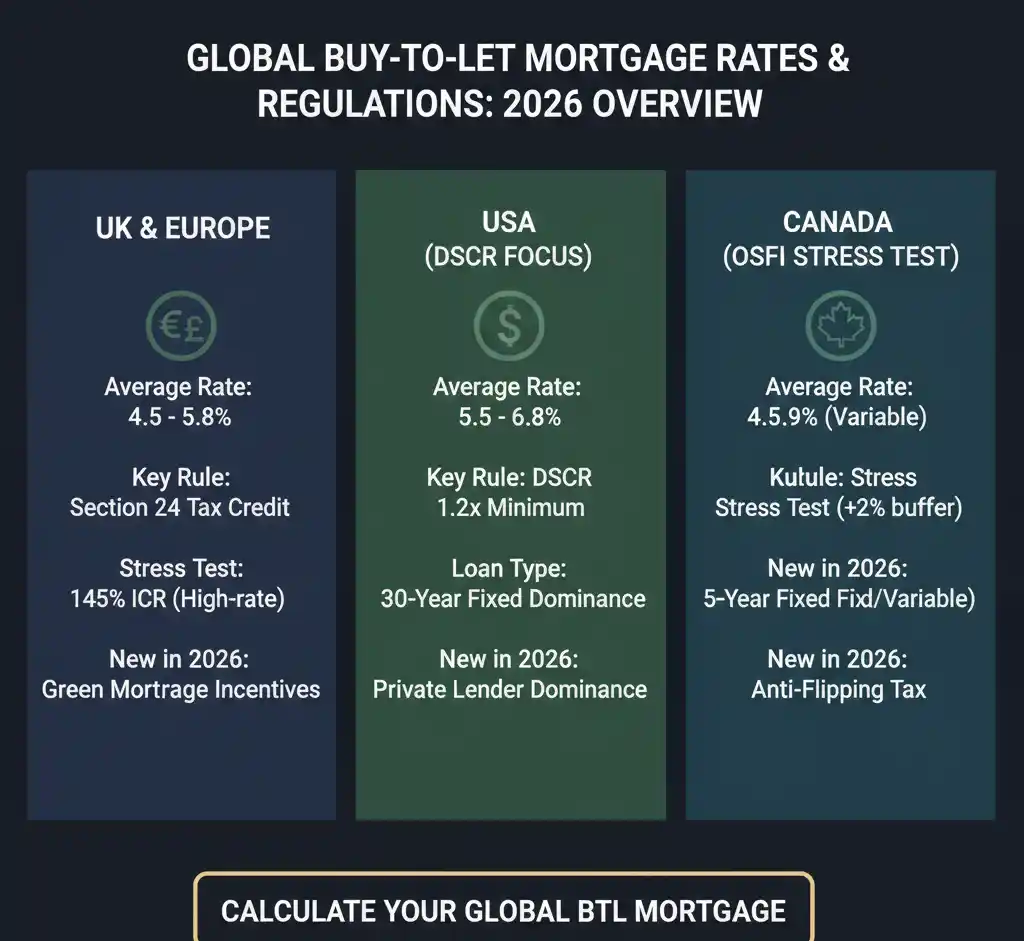

The United Kingdom: The “Section 24” Evolution

In the UK, the landscape remains dominated by the long-standing Section 24 tax changes, which have been further refined in the 2026 budget. Landlords can no longer deduct mortgage interest from their rental income before paying tax. Instead, they receive a 20% tax credit. For many, this has made the interest-only repayment model less lucrative on paper, pushing more investors toward “Limited Company” (Special Purpose Vehicle) structures. When using our Buy to Let Mortgage Repayment Calculator 2026, UK investors must ensure they are factoring in these tax slippages to avoid a “phantom profit” scenario.

The United States: DSCR and The Rise of Private Lending

In the USA, 2026 has seen a surge in Debt Service Coverage Ratio (DSCR) loans. Unlike the UK, the US market focuses heavily on the property’s ability to cover its own debt. Lenders look for a ratio—typically 1.2 or higher—meaning the rent must be 20% higher than the mortgage repayment. The U.S. Department of Housing and Urban Development (HUD) has recently updated guidelines to encourage more sustainable rental housing, which has led to more competitive rates for energy-efficient “Green BTL” properties.

Canada and Europe: The Stress Test Barrier

Canada’s “Stress Test” remains a formidable barrier in 2026. To qualify for a mortgage, your repayment capacity is tested against a rate that is often 2% higher than the actual market rate. Similarly, in European hubs like Germany and the Netherlands, rent control laws introduced in early 2025 are now in full effect, capping the maximum rent you can charge. This makes the accuracy of your repayment calculation vital; if your repayment is fixed but your rent is capped, your margins can disappear overnight.

Why Location Dictates Your Repayment Strategy

In 2026, the strategy of “Buy and Forget” is dead. Successful investors are those who adapt their repayment types based on local inflation. For instance:

- In High Inflation Zones: Fixed-rate repayments are king, as they allow you to pay back the bank in “cheaper” future currency while your rent increases with inflation.

- In Stable/Deflationary Zones: Variable rates might offer a lower entry point, but they carry the risk of “Payment Shock” if central banks pivot unexpectedly.

For real-time data on how global inflation is shifting these markets, investors often consult the International Monetary Fund (IMF) Housing Market Tracker, which provides a bird’s-eye view of where repayments are becoming most burdensome.

Advanced Risk Mitigation and Financial Engineering in 2026

To achieve a professional-grade understanding of buy-to-let mortgage repayment, one must delve into the “Financial Engineering” aspect of property management. In 2026, simply paying your monthly bill is not enough; you must optimize the debt.

1. The Impact of Compound Interest on Long-term BTL Debt

Most investors fail to realize how a mere 0.5% fluctuation in interest rates can lead to a difference of tens of thousands of dollars/pounds over a 25-year term. For instance, on a $500,000 loan, the difference between 4.5% and 5% interest over the full term can exceed $40,000 in total interest paid. This is why using the Buy to Let Mortgage Repayment Calculator 2026 for “Scenario Modeling” is vital. You should calculate for:

- The Base Case: Current market rates.

- The Bear Case: A 2% increase in rates due to sudden inflation.

- The Bull Case: A 1% decrease allowing for future refinancing.

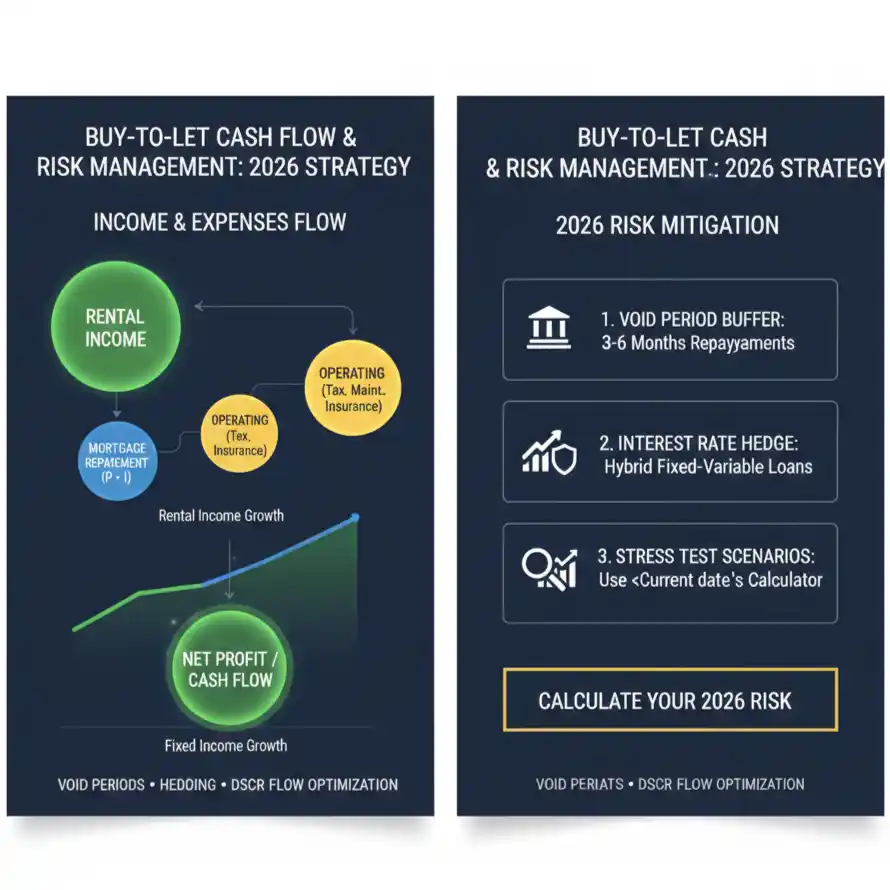

2. Liquidity Management and the “Void Period” Buffer

A “Void Period” is when your property sits empty without a tenant. In 2026, global economic shifts have caused tenant turnover rates to fluctuate. If your buy-to-let mortgage repayment is $1,800 per month, and your property is vacant for two months, you are $3,600 in the red. Professional investors utilize “Sinking Funds”—a dedicated savings account where 10% of every rent check is stored specifically to cover repayments during these gaps.

3. Tax Efficiency via Repayment Structuring

In many jurisdictions, the way you repay your loan determines your tax liability. For example, in the USA, the IRS (Internal Revenue Service) allows for depreciation of the building, but the mortgage interest deduction has specific limits depending on whether the property is held personally or through an LLC. In 2026, the intersection of repayment and taxation is where the real profit is made. If your repayment is structured as interest-only, your tax-deductible expenses might be higher, but your long-term equity growth is zero.

The Strategic Roadmap for 2026 and Beyond

As we look toward the latter half of 2026, the “Macro-Economic” factors affecting BTL repayments are shifting toward a more stabilized but higher-rate environment. To rank among the top 1% of investors, you must adopt a “Portfolio approach” rather than an “Individual asset approach.”

1. Portfolio Cross-Collateralization

Large-scale investors often use the equity in one property to lower the what is buy-to-let mortgage repayment on another. By re-evaluating your entire portfolio’s Loan-to-Value (LTV) ratio, you can negotiate “Bulk Rates” with lenders like HSBC Commercial or Chase Bank. This strategy can drop your overall interest burden by 0.75% to 1.25%, which, on a multi-million dollar portfolio, is a massive saving.

2. The Green Mortgage Revolution

A new trend in 2026 is the “Green Repayment Incentive.” If your rental property meets high energy-efficiency standards (A or B rating), many lenders are now offering “Green Mortgages” with discounted repayment rates. This not only lowers your monthly outgoings but also makes the property more attractive to modern, eco-conscious tenants, ensuring higher occupancy rates.

3. Exit Strategies and Capital Gains

Every buy-to-let mortgage repayment should be made with the “Exit” in mind. Are you paying down the capital to sell the property debt-free in 20 years? Or are you paying interest-only to keep cash flow high for a “Flip” strategy? In 2026, the capital gains tax (CGT) in countries like the UK and Canada has become a major factor in these decisions. If you pay down the mortgage (Capital Repayment), you increase your equity, which might lead to a higher tax bill upon sale, but provides a much larger lump sum for retirement.

Final Summary for the Global Investor

Mastering the art of BTL involves a constant cycle of Calculation, Observation, and Execution. By utilizing our Buy to Let Mortgage Repayment Calculator 2026, you are not just looking at numbers; you are looking at the heartbeat of your financial future. The investors who succeed in 2026 are those who treat their mortgage not as a debt, but as a lever to generate wealth.

Deep-Dive Case Study – The UK Market (2026 Resilience)

In the United Kingdom, the buy-to-let sector has faced numerous headwinds, yet it remains a primary choice for long-term wealth. To understand the buy-to-let mortgage repayment in the UK, we must look at a practical scenario.

Scenario: An investor purchases a terraced house in Manchester for £300,000 with a 25% deposit (£75,000). The mortgage required is £225,000. In 2026, the average BTL interest rate for this LTV (75%) is approximately 5.2%.

- Interest-Only Repayment: The monthly cost would be roughly £975.

- Capital Repayment: The monthly cost jumps to approximately £1,340.

If the rental income is £1,600, the interest-only model provides a healthy “Net Cash Flow” of over £600 (before taxes). However, the UK’s “Prudential Regulation Authority” (PRA) requires lenders to use a Stress Test. Even if the actual rate is 5.2%, the bank might calculate your repayment at 7% to ensure you can still pay if rates rise. This is where our Buy to Let Mortgage Repayment Calculator 2026 becomes invaluable for UK landlords to ensure they meet the Interest Cover Ratio (ICR) of 145% required for higher-rate taxpayers.

Why Investors Must Know What is buy to let mortgage repayment

“Understanding what is buy to let mortgage repayment helps you decide between interest-only and capital repayment structures. This choice directly affects your monthly cash flow and your long-term equity growth in the 2026 housing market.”

Section 7: Deep-Dive Case Study – The USA Market (DSCR Focus)

The United States market in 2026 operates differently, focusing heavily on the Debt Service Coverage Ratio (DSCR). For American investors, the repayment is less about personal income and more about the property’s performance.

Scenario: An investor buys a multi-family unit in Texas for $500,000. With a 20% down payment, the loan amount is $400,000. US 30-year fixed mortgage rates in 2026 for investment properties are hovering around 6.5%.

For a Capital Repayment (Amortized) loan, the monthly repayment would be roughly $2,528. To qualify for a DSCR loan, the property must generate enough rent to cover this repayment by at least 1.2x.

- Minimum Required Rent: $2,528 x 1.2 = $3,033.

If the property only rents for $2,800, the investor will fail the DSCR test and may need to put down a larger deposit or find a different repayment structure. This level of precision is why US investors must cross-reference their numbers with the National Association of Realtors (NAR) data and use a precise tool to calculate their potential monthly liabilities.

Section 8: Deep-Dive Case Study – The Canadian Market (Stress Test & Variable Rates)

Canada’s 2026 market is defined by the “Office of the Superintendent of Financial Institutions” (OSFI) and its rigorous stress tests. Even if you secure a mortgage at 5%, you must prove you can afford the buy-to-let mortgage repayment at 7%.

Scenario: A condo investment in Toronto for $700,000. With a 25% deposit, the mortgage is $525,000. In Canada, many investors use 5-year fixed terms renewed periodically.

If the investor chooses a variable rate, they face the risk of “Trigger Rates.” If the interest rate rises to a certain point, the monthly repayment may not even cover the interest, causing the principal balance to actually increase. This “Negative Amortization” is a major risk in 2026. Canadian investors use our Buy to Let Mortgage Repayment Calculator 2026 to set “Trigger Warnings” for their portfolios, ensuring that even if the Bank of Canada raises rates, their repayments remain manageable within their rental income limits.

“In summary, mastering the concept of what is buy to let mortgage repayment is the key to building a sustainable property portfolio. It allows you to plan for tax changes and interest rate hikes across the UK, USA, and Canada effectively.”

Frequently Asked Questions (FAQ)

What is buy to let mortgage repayment?

It is a monthly payment made by a property investor to a lender. It can be interest-only (paying only the interest) or capital repayment (paying interest plus the original loan amount).

How much rent do I need for a BTL mortgage?

Typically, your rental income must be 125% to 145% of your monthly mortgage repayment. This is known as the Interest Cover Ratio (ICR) and is a standard requirement in 2026.

Is interest-only BTL cheaper monthly?

Yes. Interest-only repayments are lower each month because you aren’t paying back the borrowed capital. This maximizes your monthly rental profit but leaves the original debt unpaid.

Can I get a 90% LTV buy to let mortgage?

No. In 2026, most BTL lenders require a minimum deposit of 20% to 25%. A 75% LTV is the industry standard for securing competitive repayment rates.